How PIRE Was Born — The Catastrophe and the Rebuild

Part one of three on Porch Group (PRCH)

In the autumn of 2021, Porch Group’s stock hit $27.50. By late 2023 it had fallen to under $0.50. That is a 98% decline from peak to trough — the kind of number that shows up on lists of pandemic-era wreckage alongside companies that no longer exist.

Porch does exist, though its transformation from a fragile, catastrophe-exposed insurer into a capital-light insurance platform with proprietary housing data and embedded distribution advantages is still widely misunderstood.

Introduction To Porch

Porch Group was founded in 2012 by Matt Ehrlichman. The company launched Porch.com in 2013 as a home services marketplace and spent the following years building software — not consumer-facing software, but the back-office platforms used by the companies that interact with homeowners at the most consequential moments of the home transaction. By the time Porch listed on NASDAQ in 2020 via a SPAC merger, it had assembled a position in three complementary businesses that would prove to be the foundation of everything that came later.

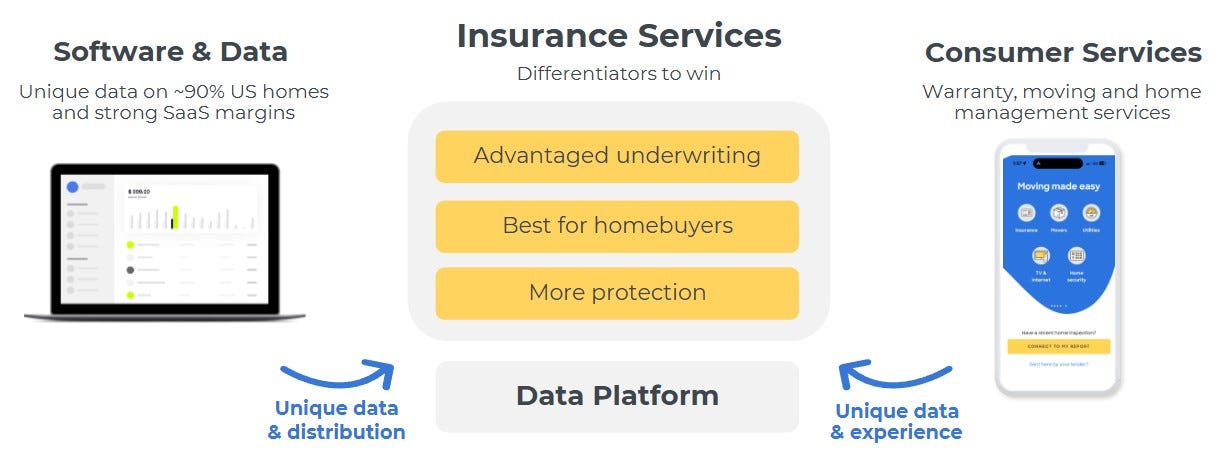

Software & Data. The first and most strategically important arm is the software platform. Porch owns a range of B2B software businesses which work in the housing sector. With just two of its offerings, Porch handles more than 40% of all home inspections carried out in the US each year and commands a similar market share among title companies. The strategic value of these positions is that every inspection, every title transaction, every policy application generates structured data about a specific property at a specific point in time. Today, Porch is a business with “insights into nearly 90% of properties in the US to understand property attributes and conditions of homes”.1

Consumer Services. The second arm encompasses the warranty business, a moving concierge service, and assistance with home set-up (TV, internet, security). These services generate transactional revenue linked to home purchase volumes while also providing access to consumers at the point of home purchase.

Insurance Services. The final arm is the insurance business — now centred on PIRE and its fronting carrier HOA, described in detail below. The strategic logic was that advantaged data, low-cost distribution embedded in the home transaction, and a differentiated consumer experience could together build an insurance carrier with structural loss ratio advantages over traditional competitors.

That is the strategic architecture Porch spent the first decade building. When it listed in 2020 with $72 million in revenue, the insurance business was, in Ehrlichman’s own description, “just part of the strategy.” By 2024 it would be the centre of it. The journey between those two points was considerably more turbulent than could have been foreseen.

The Perfect Storm

Between 2022 and 2023 the business experienced multiple shocks simultaneously. Any one of them would have been painful. Together, they were nearly fatal.

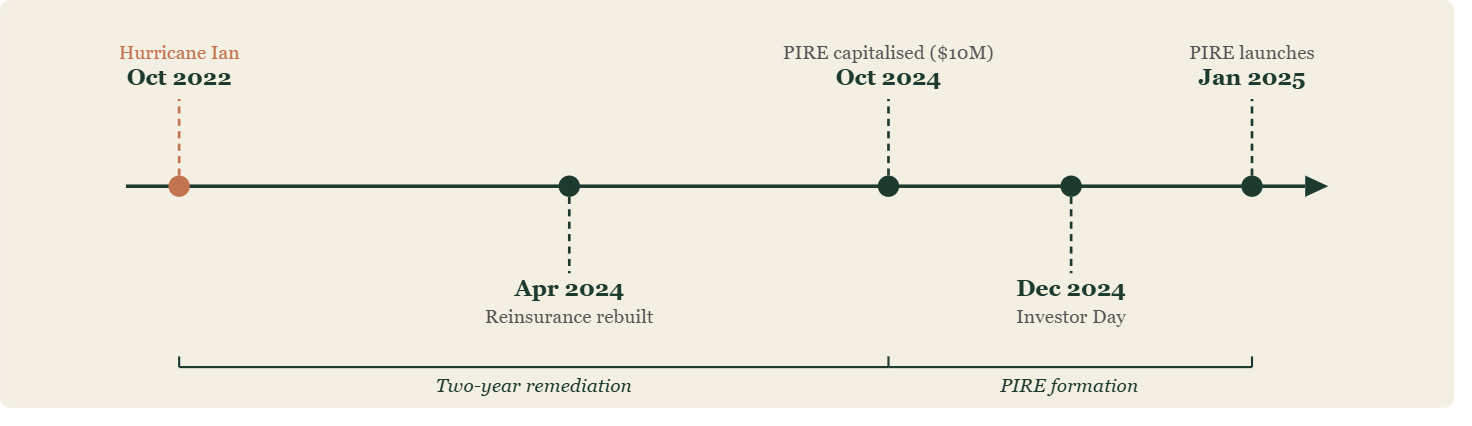

The insurance implosion. The insurance business was hit first and hardest. In October 2022, Hurricane Ian made landfall in South-west Florida as a Category 4 storm, producing over $100 billion in insured industry losses. HOA had meaningful Florida exposure and was catastrophically underpriced for what it faced — a problem compounded by the inflation that had been running through construction and replacement costs since 2021. HOA had grown rapidly into a market where the real cost of claims was rising faster than the premiums it was collecting; Ian simply brought the reckoning forward. By the full year 2023, HOA’s net loss ratio had reached 122.9% — losing $1.23 for every dollar of premium collected after reinsurance, through a reinsurance programme that itself proved inadequate.

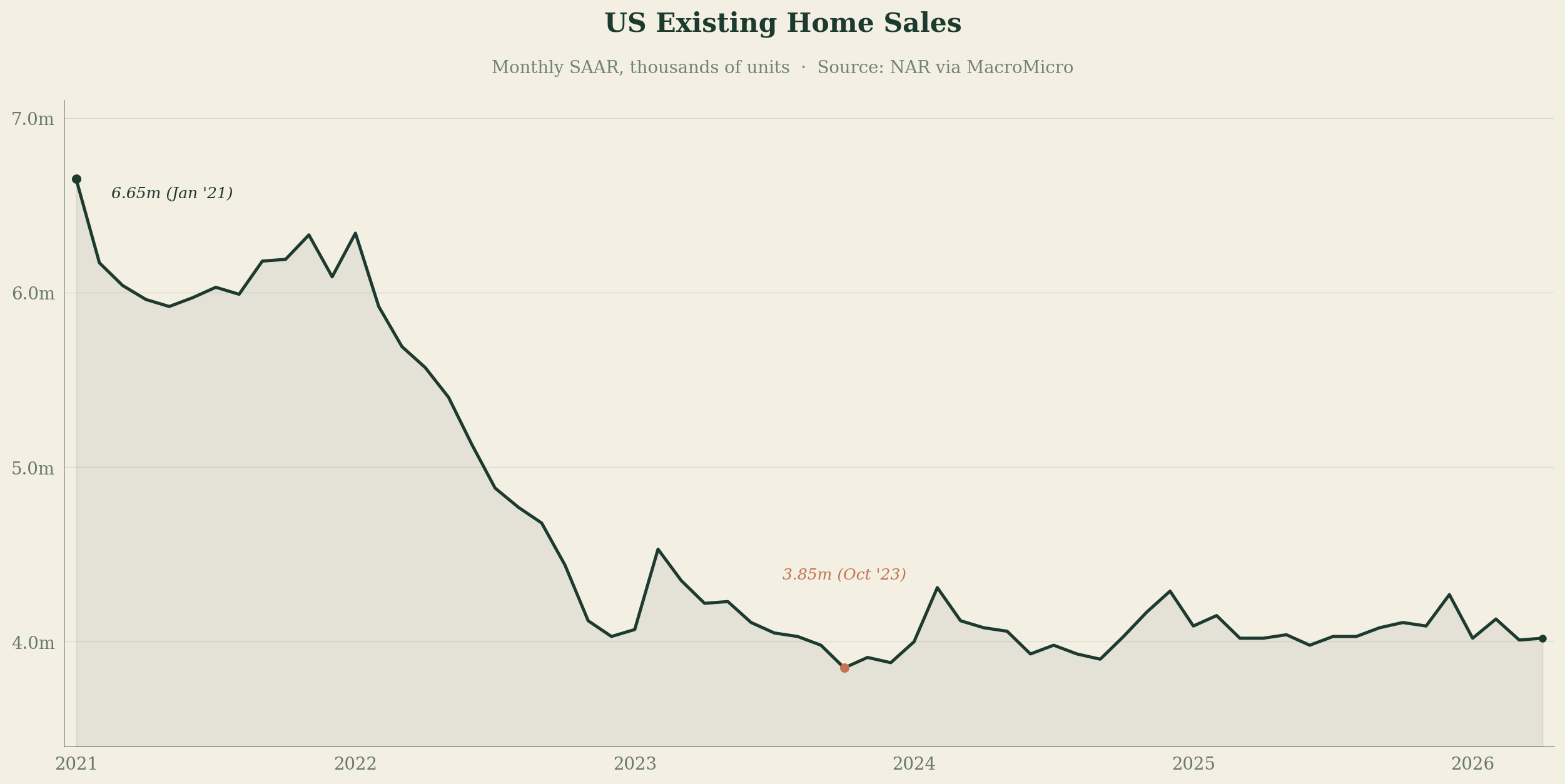

The software collapse. The software business, which should have provided a buffer, was simultaneously collapsing. The Federal Reserve began raising rates aggressively from early 2022, roughly doubling mortgage rates within a year. US existing home sales fell from an annualised rate of over 6.5 million in 2021 to around 4 million by late 2022 — and stayed there. Porch’s software businesses serve home inspectors, moving companies, and warranty providers, all of whose revenues are almost entirely tied to housing transaction volumes. Both legs of the business deteriorated at the same time, and the debt Porch had accumulated through acquisitions in 2020 and 2021 — taken on at peak valuations to build out the software platform — became existential as cash generation fell away.

The market’s verdict. The market did not wait for the situation to resolve. Investors who had bought Porch as a high-growth software company with an insurance optionality story were now looking at catastrophic insurance losses, collapsing software revenue, and a balance sheet that could not easily absorb either. The stock, which had traded above $27 in late 2021, fell below $0.50 by late 2023 — the 98% decline referenced at the start of this article. It was not a market overreaction. It was a rational assessment of a business in genuine distress, with multiple shocks arriving at once and no obvious route through them.

How Management Reacted

The two-year rebuild. Management responded to this disaster by, first and foremost, fixing the insurance book while it remained inside the old structure. The remediation had four components, all running in parallel. HOA raised rates aggressively wherever and whenever regulators permitted — slower than it sounds, given that each state requires actuarial justification and approval, but in Texas, where the operational leverage was greatest, the increases came through. Simultaneously, the book was deliberately shrunk. HOA pulled back from Florida and other high-risk markets, throttling the agency distribution channel that had been running at roughly 650 active agents writing 125,000 new policies per year. The reinsurance programme was rebuilt from scratch after the previous structure had proved inadequate when Ian arrived. Finally, across the group headcount and operational costs were cut, with the software and consumer services businesses managed for margin rather than growth.

The results. By end of 2024, the results were visible. HOA’s statutory surplus had recovered to approximately $100 million — a record, and double the prior year. It was at this point, once the book was sufficiently clean to be worth placing into a structurally superior vehicle, that the PIRE formation proceeded.

What the rebuild left unresolved. The sequence matters for how you assess the current results. The underwriting numbers now reported against PIRE were generated by a book management had already spent two years repairing before PIRE existed. They are the combined product of the remediation and the structural solution. The remediation proved the underwriting model could work. PIRE is the vehicle through which it scales. What neither the remediation nor the restructuring resolved is the debt the crisis left behind — over $475 million of convertible notes, carrying an effective interest rate as high as 17.9%. The insurance engine has been rebuilt. The balance sheet has not. That remains the single most important unresolved question in the thesis, and it is addressed in the final part of this series.

What PIRE Actually Is

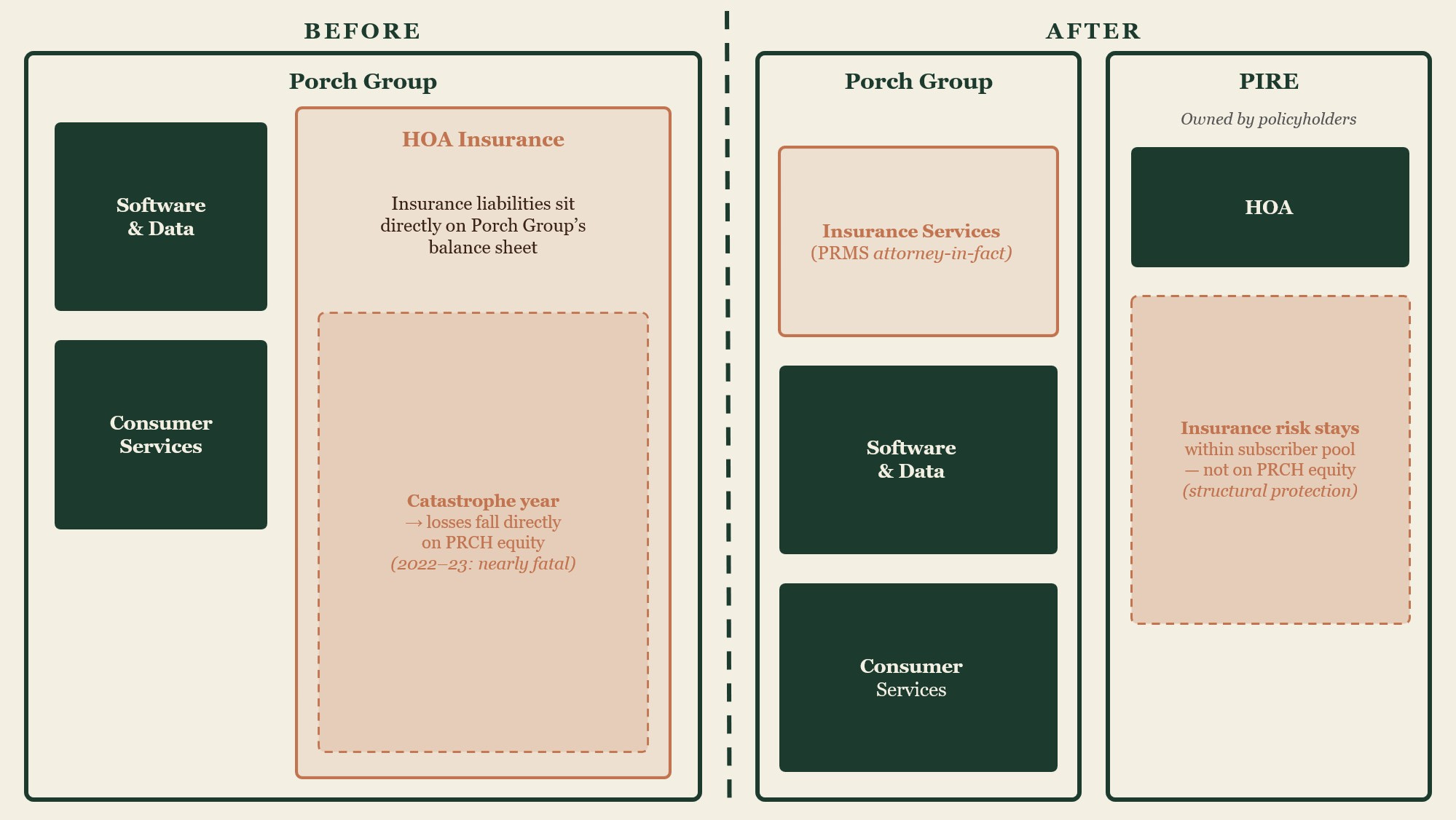

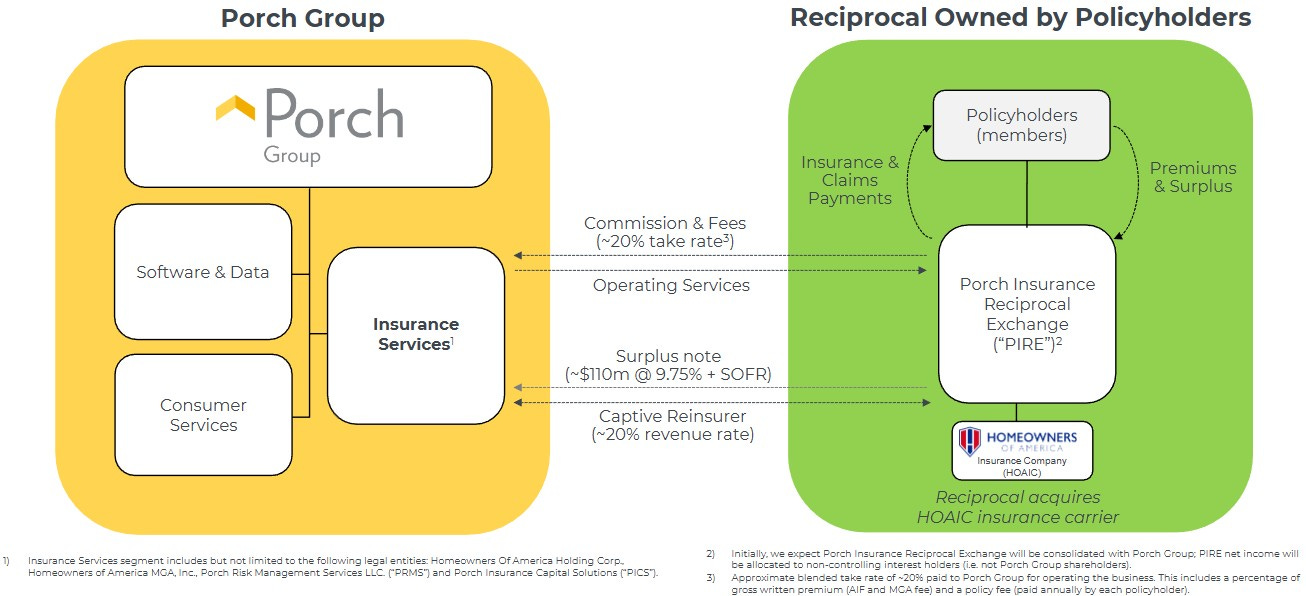

The subscriber model. Porch Insurance Reciprocal Exchange (”PIRE”) is a reciprocal exchange organised under the Texas Insurance Code. This legal form is old. Reciprocals have existed in the United States since the nineteenth century. The economics are distinctive. A reciprocal exchange is owned by its policyholders, who are called subscribers. When you take out a policy with a reciprocal, you become a subscriber — a participant in a mutual arrangement where all subscribers agree to share each other’s insured risks. The exchange itself is not a corporation owned by shareholders; it is a collective vehicle owned by the people it insures. Profits and losses accrue to the subscriber pool, not to outside equity holders.

The attorney-in-fact. The exchange is managed by an attorney-in-fact, an entity appointed by the subscribers to handle underwriting, operations, and investment. In PIRE’s case, the attorney-in-fact is PRMS (Porch Risk Management Services), a subsidiary of Porch Group. PRCH does not own PIRE. It manages PIRE for a fee. That distinction is the entire point. By moving the risk-bearing entity into a subscriber-owned reciprocal managed by (but not owned by) Porch Group, the structure separates what had previously been conflated. PIRE carries the insurance risk. Its capital (”statutory surplus”) belongs to the subscribers. If PIRE has a bad year, the losses sit within the subscriber pool. Porch Group’s P&L recognises revenue tied to the gross premiums written by PIRE in any given period as well as their software and consumer services businesses. The catastrophic downside of a severe insurance loss year no longer falls directly onto the PRCH balance sheet.

How PRCH benefits. Porch Group makes money from PIRE in three distinct streams. The first is the operator fee. Through PRMS, PRCH charges PIRE approximately 20% of gross written premium for providing all operating services: underwriting, claims management, agency distribution, and the full corporate infrastructure. The second is captive reinsurance. PRCH provides non-catastrophe quota share reinsurance to PIRE, earning c.20% of gross written premium. Finally, there is interest on the surplus notes. When PRCH sold HOA to PIRE in January 2025, it received $105.8 million in surplus notes in return — three tranches, all at SOFR plus 975 basis points. Surplus notes are treated as equity on PIRE’s statutory balance sheet, which is precisely why they were used to capitalise the exchange. For PRCH, they are debt instruments generating interest income. Payment requires approval from the Texas Department of Insurance, so this stream is not guaranteed in any given period — but it accrues contractually and is a meaningful component of the long-run return on the capital PRCH injected.

A note on the accounting. Because PRCH manages PIRE as attorney-in-fact, accounting rules require PIRE’s results to be consolidated into PRCH’s GAAP financial statements — meaning the revenues and losses of an exchange owned by its policyholders appear on the income statement of a company that does not own it. Porch Group’s non-GAAP framework, Porch Shareholder Interest (PSI), strips the Reciprocal back out to show only the economics that accrue to PRCH equity holders; it is PSI, not the consolidated GAAP figures, that is the correct lens for valuing the listed shares. There is also a circular element to the structure — PIRE holds 18.3 million PRCH shares on its balance sheet — the implications of which are worth understanding and will be covered in the valuation article.

Why It Mattered

Before PIRE. The PIRE structure was not cosmetic. It changed the fundamental risk profile of the listed entity. Before the restructuring, PRCH was, in economic terms, an insurance company with a software business attached to it. Insurance liabilities sat on the holding company balance sheet. A catastrophic loss year, and 2022–2023 proved how quickly one could arrive, could produce staggering losses. The equity was exposed to a tail risk that no amount of software growth or operational improvement could fully hedge. That is a difficult proposition to own for any investor with a finite tolerance for catastrophic downside.

Capital-light by design. After PIRE, PRCH is a capital-light operator that extracts management economics from an insurance exchange it runs but does not own. The subscriber pool carries the insurance risk. PRCH collects fees, reinsurance spreads, and note interest. The structure is not immune to downside — the operator fee scales with premium volume, so a business-threatening event at PIRE would reduce the fee base — but the existential exposure is gone. For the first time, the equity can be assessed on its own merits rather than in the shadow of potential insurance catastrophe.

The thesis, finally visible. That matters because it allows investors to focus on what Ehrlichman and his team were actually building all along. The underlying thesis, articulated even before Porch.com launched in 2013, was never primarily about being an insurance carrier. It was about building a data advantage over US homes that no traditional carrier could replicate, then using that advantage to underwrite better, price more accurately, and select lower-risk policyholders at the moment of home purchase. The data platform, the 40% share of all US home inspections, the insights into nearly 90% of US properties — these were always the foundation. Insurance was the commercial expression of the advantage, not the business in itself. The old structure, where insurance catastrophe risk sat directly on the holding company, obscured that distinction and made the business nearly impossible to own through a difficult weather year. The new structure does not.

Whether the data advantage is as real as the thesis claims — whether it produces a structurally lower loss ratio through cycles, not just favourable weather quarters — is the question the statutory filings begin to answer. That is what the next part of this series examines.

Next: Reading the Insurance Engine.

Patient Money publishes investment research for informational purposes only. Nothing here constitutes financial advice or a solicitation to buy or sell any security. Always do your own research and consult a financial adviser before making investment decisions. The author holds a position in PRCH at the time of publication.

Nicole Pelley — EVP & GM, Porch Platform — Porch Group Investor Day, December 2024